Quick, easy, secure & seamless

Create Your Free Account

Take advantage of our low fees, low spreads, low prices, and feature-packed app to unlock your trading & investing potential today.

Get startedWritten by Swyftx

If you’re living in New Zealand and hold BTC, ETH, or any other type of digital asset, you’ve probably heard about crypto taxes, but may be unsure how it will affect you.

Well, the good news is that spot trading crypto taxes in New Zealand can be straightforward depending on your activities. Different tax obligations exist depending on your residency status and crypto activity. This article provides a high-level summary of cryptocurrency taxes in New Zealand to help you understand what they entail so that you don’t get caught out come tax time.Some aspects of crypto taxation can be complex or uncertain. This article is prepared to give you an outline of the general principles applying to taxation of crypto assets in New Zealand. There are some types of crypto activities that may have more complex treatment (such as certain types of “DeFi” transactions or crypto lending options) that are not covered by this article.

This publication is brief and general in nature. It is provided for education only and has not been prepared by a lawyer regulated by the Lawyers and Conveyancers Act 2006. If you need assistance with tax matters, you should seek professional tax advice from your legal, tax and/or financial advisor in relation to the matters dealt with in this publication.

Cryptocurrency itself has only been around for the blink of an eye – fiscally speaking. Founded in 2009, Bitcoin was the first cryptocurrency in existence. Since then, it has seen worldwide adoption and also paved the way for a number of other popular cryptocurrencies like Ethereum (ETH), Binance Coin (BNB), Cardano (ADA) Dogecoin (DOGE) and many more. For many years, the tax and legal treatment of cryptocurrencies was very uncertain but from around 2017 the Inland Revenue Department (IRD) started actively considering the taxation of crypto assets and has published some commentary on key aspects.

New Zealand’s Inland Revenue Department does not view cryptocurrency as money. Instead, it is viewed as property for tax purposes. There are no crypto-specific tax laws in place although new legislation is currently before Parliament to clarify the GST treatment of “crypto assets” along with some timing issues. The term crypto assets is broad and includes all types of cryptocurrencies and non-fungible tokens (NFTs).

Although New Zealand does not have a comprehensive capital gains tax (CGT), it’s important to be aware that any profits or losses made on the sale of crypto will generally be taxable at your applicable marginal income tax rate.

There is a common misconception that cryptocurrencies like Bitcoin are anonymous. These coins are decentralised, meaning they are not controlled by a central bank or government, so you could be forgiven for thinking that your crypto assets will never cross the IRD’s radar. However, this is not the case.

As part of its crackdown on crypto investors, the IRD began requesting that cryptocurrency exchanges share crypto transaction data with the department. This will enable the IRD to more accurately identify crypto investors for tax purposes, and crypto assets assessed as part of their personal income.

As part of this, exchanges have been requested to supply details to the IRD relating to individual’s personal details as well as the specific type of and value of their cryptocurrency assets. Those details will also likely include the wallet addresses you may have used to deposit crypto assets which in turn may reveal further information as to your activities.

As cryptocurrency is treated as property for individuals, any profits are usually subject to tax on disposal. According to the IRD, disposal can be classified as:

There may be circumstances where you “dispose” of your crypto without realising you have made a disposal – for example, IRD considers that depositing to some crypto lending platforms may involve a disposal for tax purposes, particularly when you receive a token in exchange.

Whether you are a trader or an investor, the IRD will assess profit from both activities as taxable income.

As reported by the IRD, if the purpose of acquiring a crypto asset is to sell or exchange them, you’ll be required to pay income tax when you do. Alternatively, if you incur a loss when you sell or exchange crypto assets, you may be able to claim this as a loss.

The IRD also stated that the tax is also applied when swapping one cryptocurrency for another.

New Zealand’s tax obligations differ slightly for residents, non-residents and new and returning residents. This also applies to cryptocurrency taxes. If you aren’t sure as to whether you are a resident for New Zealand tax purposes, it’s important to speak with a qualified professional who can guide you as tax residency rules are complicated.

As a non-resident for tax purposes in New Zealand, you are usually taxed only if you have New Zealand-sourced income and gains. The tax concept of “source” for crypto purposes is not fully developed so there are some uncertainties here. While this might include crypto assets that are held in NZD or traded for NZD, most countries have double tax agreements with each other and usually these types of profits are taxed only in the person’s home country.

Any crypto income generated from assets mined or sold outside of New Zealand are not subject to New Zealand tax for non-residents.

For new and returning residents, there is a four-year ‘grace period’ where residents may be classed as transitional tax residents. New and returning residents are constituted as new residents for tax purposes or those who have returned after ten years.

In this period, you do not have to pay tax on a majority of types of offshore income. There may be an argument that this includes crypto assets which were acquired while outside New Zealand where there is no New Zealand connection. We are aware that the IRD is considering rulings on this point but for now this is a grey area.

Even if that exception can apply to crypto assets – tax will still apply to income with a source in New Zealand (for example, gains made from trading activities carried out in New Zealand), or employment income that is foreign-sourced (eg. residents getting paid in cryptocurrency from an overseas employer).

In New Zealand residents are taxed on their worldwide income. This includes crypto assets that are held in NZD or traded for NZD.

When it comes to crypto assets, residents are taxed on buying and selling crypto assets, and mining crypto assets.

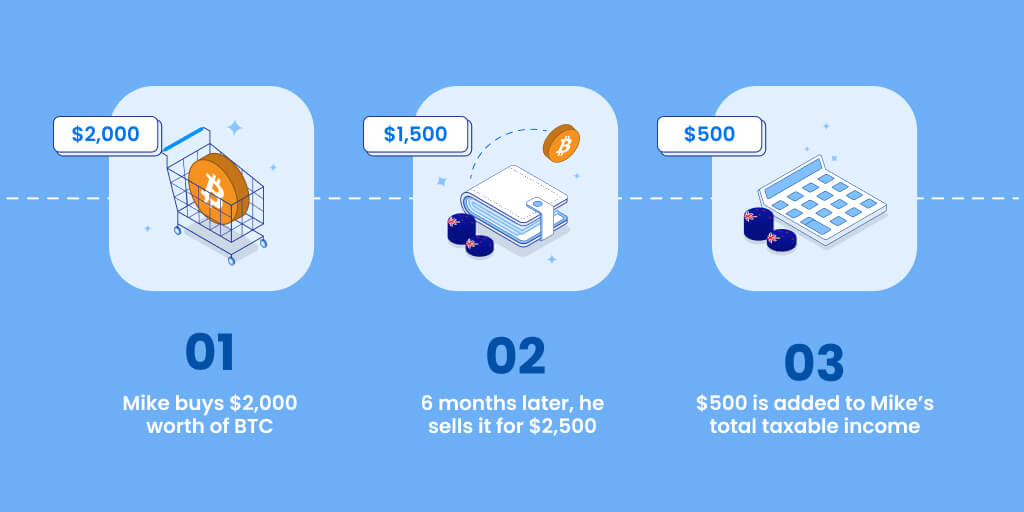

When an individual in New Zealand sells cryptocurrency for a profit, certain taxations apply. You must pay income tax on your profits, just like you would if you ran a business, or traded on the stock market.

It is important to note, this tax does not apply unless you dispose of your cryptocurrency. If, however, you exchange your cryptocurrency from BTC to ETH (or any other coin), any profits made at that point become taxable. You do not need to cash out to NZD to create a tax obligation. You will need to find out what the BTC worth was in fiat currency (NZD) when you bought it and what the ETH worth was when you made the trade. The difference between those fiat currency amounts is subject to tax.

If you’ve made a loss when buying and selling cryptocurrency, you can offset your loss against any income you’ve made over the year (including PAYE income deducted from wages or salary).

When you go to do your tax return once the tax year has ended (March 31st) you’ll need to complete and file an individual tax return (IR3). Make sure to use the “Other Income” section of your return when reporting crypto trading gains and losses.

Cryptocurrency tax laws are subject to change due to new changes in legislation or court decisions; always check the IRD website for up-to-date information.

If your primary business activity involves any of the following, you are likely classed as a crypto business:

Even if your business does not undertake these activities, you’re subject to tax if you receive or pay cryptocurrency for services.

In New Zealand if you accept crypto assets as a form of payment for goods and services, you will need to pay tax on them.

In New Zealand, accepting crypto as a form of payment is referred to as a barter transaction. Ensure you calculate their fiat value in NZD at the time they were received to work out your taxable income. If you are GST registered, you must return GST on that sale as if you had received the equivalent value in NZD.

If you then sell these assets, any profit you make is also taxable.

A draft tax bill currently proposes that crypto assets will be exempt from GST (when sold) but non-fungible tokens (NFT) have been excluded from this exemption.

Businesses who accept Bitcoin: If you’re a business who accepts Bitcoin payments, request to get added to our index.

An employer may choose to pay their workers in crypto assets. When paying employees with cryptocurrency rules around Fringe Benefits Tax (FBT) and Pay As You Earn (PAYE).

You can view the IRD’s Public Rulings to work out whether PAYE and FBT apply to your situation.

Staking cryptocurrency is the practice of using your coins to support the operation of and verifications on a blockchain network, and in exchange you could receive rewards for supporting the network.

The value of these rewards can vary depending on the cryptocurrency and how much is staked.

Just like any other income, staking income from crypto is subject to tax in New Zealand when it is earned. If the value increases from the date of receipt until the date of disposal, those additional gains will also be taxed.

A person holds ten of Coin A coins, with a market value of $10 each (total value of $100) and they staked their coins. In the process they earn another 5 coins. For the sake of the example, we’ll assume market value doesn’t change.

They now have $150 in value and have made $50 profit in staking. The $50 of staking is taxed at each point coins are received.

If the value drops or rises from the date of receipt to the date of disposal, that is another taxable event. For example, if the coins doubled in value, the staking rewards would now be worth $100 and the additional $50 would be taxed on disposal.

When you give cryptocurrency as a gift to a friend or family member, it’s like selling it in the eyes of the Inland Revenue Department. So, you will likely need to pay tax on it, even if you don’t get anything in return.

In New Zealand, if you get cryptocurrency as an airdrop, it could be taxed when you receive it, when you dispose of it, or both. Whether or not you have to pay tax depends on the circumstances surrounding the airdrop.

If you receive an airdrop as part of a business, for a profit-making scheme, or in exchange for services, you will have to pay tax when you receive it. But, if the airdrop does not fall into any of these categories, you will not have to pay tax at the time of receipt. However, the crypto asset you receive will have a cost basis of zero, so you will have to pay tax on the full amount when you dispose of it later.

If you acquire the cryptocurrency with the intention of selling it later, or dispose of it as part of a profit-making scheme, you will have to pay tax at the time of disposal.

It can be complicated to determine whether or not an airdrop is taxable, so it’s best to read the publication QB 21/06 from the IRD for more information.

When it comes to the tax treatment of cryptocurrency, any income you make from mining is also subject to tax. Better news, many of the costs you incur can be written-off. It is important to note that the IRD has explicitly outlined that hobby mining is typically taxable as a business or profit making scheme.

According to the IRD, mining is considered a profit-making scheme or business activity, and as such, you need to account for it in your tax returns. Profits and losses from cryptocurrency mining are considered assessable or deductible income.

Importantly, IRD’s view is that you may be taxed at two points in time. First, when you received the mined cryptocurrency (taxed on the value at that time) and second, when you dispose of that cryptocurrency (if it has gained in value since then).

You can claim a tax deduction for most of the costs you incur when mining crypto as a business. This includes things like your computer hardware, electricity and internet costs. Your accountant or tax agent can help you work out exactly what you can claim.

Any activity you undertook involving cryptocurrency that involved a profit or loss of fiat currencies is likely to be subject to tax.

Therefore, any activity that involved cryptocurrency creating taxable income needs to be declared.

Importantly, you will need to calculate the NZD value of your crypto assets and work out your gain or loss on each transaction. If you only sell some of a particular type of crypto asset, you will need to consider using a first in first out (FIFO) method or calculating the weighted average cost (WAC) of the investment.

For crypto assets held as an investment, any increase in value since the asset was acquired is taxable when disposed of. This also applies to crypto assets used in a business.

You will need to declare all this information on your tax return and if you’re not sure what to do, speak to an accountant.

The records you should keep include:

Use this guide:

https://www.ird.govt.nz/crypto assets/taxing/income-expenses/stolen

When filing your tax return, you might be eligible to claim a loss if any of your crypto assets were stolen.

You can claim a tax loss for the amount initially paid for them in this scenario, though you will need to supply evidence.

How do I get my info from Swyftx?

If you’re a Swyftx user, you may create and download a tax report using both the Swyftx desktop and mobile application.

For a step by step guide on how to do this, check out the following articles:

If you’re having trouble with generating your tax report or have any more questions on how cryptocurrency is taxed in New Zealand, you can reach out to our online live support.

The information provided in this article is purely factual in nature and does not constitute tax advice, financial product advice or legal advice. The information is not, nor is it intended to be, comprehensive or a substitute for professional advice on specific circumstances. The examples given do not apply to your specific circumstances.

Koinly is a tax calculator for cryptocurrency purchases and portfolio tracking tool that caters to investors and traders at all levels. As a tax calculator, Koinly is able to do a bunch of time saving reporting activities as well as indicate the potential tax implications of future activity. Just input your Swyftx transaction data (via API or CSV file upload) to identify your taxable transactions, as well as the type of tax that applies according to the ATO crypto tax rules.

Koinly will identify your cost basis, calculate your short and long-term capital gains and losses, and the fair market value of any crypto income in AUD on the day you received it.

Finally, Koinly generates an ATO compliant tax report which covers Swyftx and any other wallets you’ve synced, ready for download and filing.

Go to Koinly and get 20% off your next Crypto Tax report – ends March 31st.